For many drivers, car insurance is a mystery box of monthly premiums and legal jargon, until the moment they actually need it. Whether you are driving a brand-new electric vehicle or keeping a reliable vehicle on the road, a one-size-fits-all policy rarely suits everyone.

To protect your wallet and your peace of mind, you need to look beyond the basic premium. Here is a breakdown of the different types of car insurance you should know about to ensure you are never left footing a massive bill alone.

What is Car Insurance

Car insurance is a type of insurance that protects you financially from losses due to accidents, theft, or damage to your vehicle. It covers costs for repairs, injuries, and liability to others with different types of coverage. Car insurance is legally required in most places and provides a safety net against major financial burdens.

How Car Insurance Works

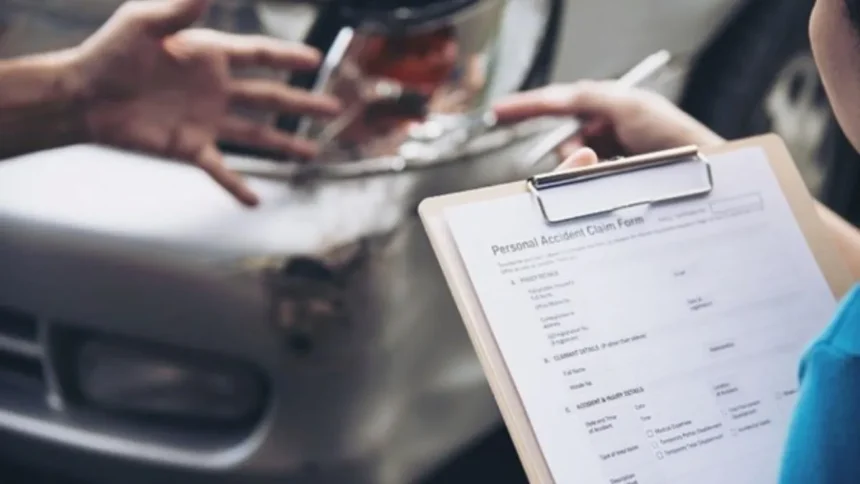

Car insurance works as a contract, and you pay as an insurer for financial protection against accidents or damage. Once you purchase a policy, premiums are usually paid monthly or quarterly. Some insurances have a deductible, an amount to be paid before the insurance company starts paying.

- You pay premiums: The insurer makes regular payments to the insurance company.

- Incident happens: An accident happens, or your car is stolen, or there is any damage to your car.

- You file a claim: You contact your insurer to report the incident and start the claim process.

- Assessment: An adjuster evaluates the damage and verifies the claim against your policy.

- Payment: If approved, you pay your deductible, and the insurer pays the remaining covered costs, often directly to the repair shop.

Types of Car Insurances

Before you get a car insurance quote, understanding the following types of insurance is crucial:

- Bodily Injury Liability

It is the type of insurance that pays for medical costs for injuries to the other person if you are found at fault.

- Property Damage Liability

It pays for damage caused to other people’s property in an accident you cause.

- Collision Coverage

If you are involved in an accident with another vehicle or object, it pays to repair or replace your car.

- Comprehensive Coverage

It covers damage to your car from non-collision events like theft, fire, vandalism, or hitting an animal. This coverage helps to pay for the repair or replacement of the vehicle.

- Uninsured and underinsured Motorist

It provides coverage if you hit a driver who is not insured or doesn’t have enough insurance to pay costs. It also covers hit-and-run accidents or injuries if you are hit by a car while walking or riding.

- Personal Injury Protection

It is the insurance policy that pays for medical bills for you and your family. It covers injuries, lost wages, and funeral expenses, regardless of fault.

How to Choose the Right Insurance Coverage

- Assess Your Needs

Vehicle Value: For new or expensive cars, comprehensive/collision is often worth it; for older, lower-value cars, third-party might suffice.

Driving Habits: Daily commuters or frequent long-distance drivers face more risk and may need fuller coverage.

- Compare Quotes

Get Multiple Quotes: Prices vary significantly between companies for the same coverage.

Compare More Than Price: Look at policy limits, deductibles, included features, exclusions, and claim settlement ratios.